How a Data-First Strategy Helped Focus Bank Enter the Fintech Space Smoothly

Client Snapshot:

Focus Bank: https://www.focusbank.com/

Bank size: $861.5M

Headquarters: Charleston, Missouri

Branches: 9

Fintech ecosystem: Sponsor bank for 2 fintechs, scaling in 2026

Focus Bank Mission

To deliver exceptional financial services by seeking insight from our clients, exceeding shareholder expectations, empowering our staff to achieve personal and professional goals, and making a difference in our communities.

Focus Bank Vision

Built on a 94-year foundation of successful community banking, FOCUS Bank is moving forward with an innovative mix of old-fashioned, first-name basis customer service combined with state-of-the-art banking products and services. This commitment to customer service, along with a sharply focused vision for the future, is proving to be a winning combination in communities throughout Southeast Missouri and Northeast Arkansas.

Challenge: Reactive vs. Proactive

Most banks are trying to modernize their data stack at the same time they’re expected to monitor a program that’s already generating customers. Internal teams are learning new responsibilities, but regulators expect precision before the bank has the tools to achieve it.

The result is that feeling of building the bike while you ride it. Someone bolts on the handlebars, adjusts the chain, rewires the brakes, and swaps the tires for something sturdier — but everyone is moving, whether the bike is ready or not.

Focus Bank’s advantage was its refusal to ride that bike. Instead, the leadership team built the data foundation and operational focus before bringing the first fintech partner online.

Kayla Jones, Chief Fintech Banking Officer for Focus Bank, said the framework-first approach is what kept the bank out of the reactive scramble that drives most fintech-sponsoring banks into manual workarounds and regulatory blind spots.

Approach: Planning for Risk and Regulation

Focus Bank had a head start. The leadership team and board had been banking high-risk verticals — cannabis since 2020 — so they were already used to the heightened oversight that fintech would bring. Their primary concern wasn’t whether they could handle scrutiny. It was knowing exactly what examiners would ask for.

Jones said the team knew from day one what examiners would scrutinize: clear KPIs, demonstrated ROI, transparent monitoring, and how each one impacts the bank.

They also accepted early that manual processes wouldn’t survive the volume of data a fintech program produces. The days of running everything from a spreadsheet, Jones said, were over.

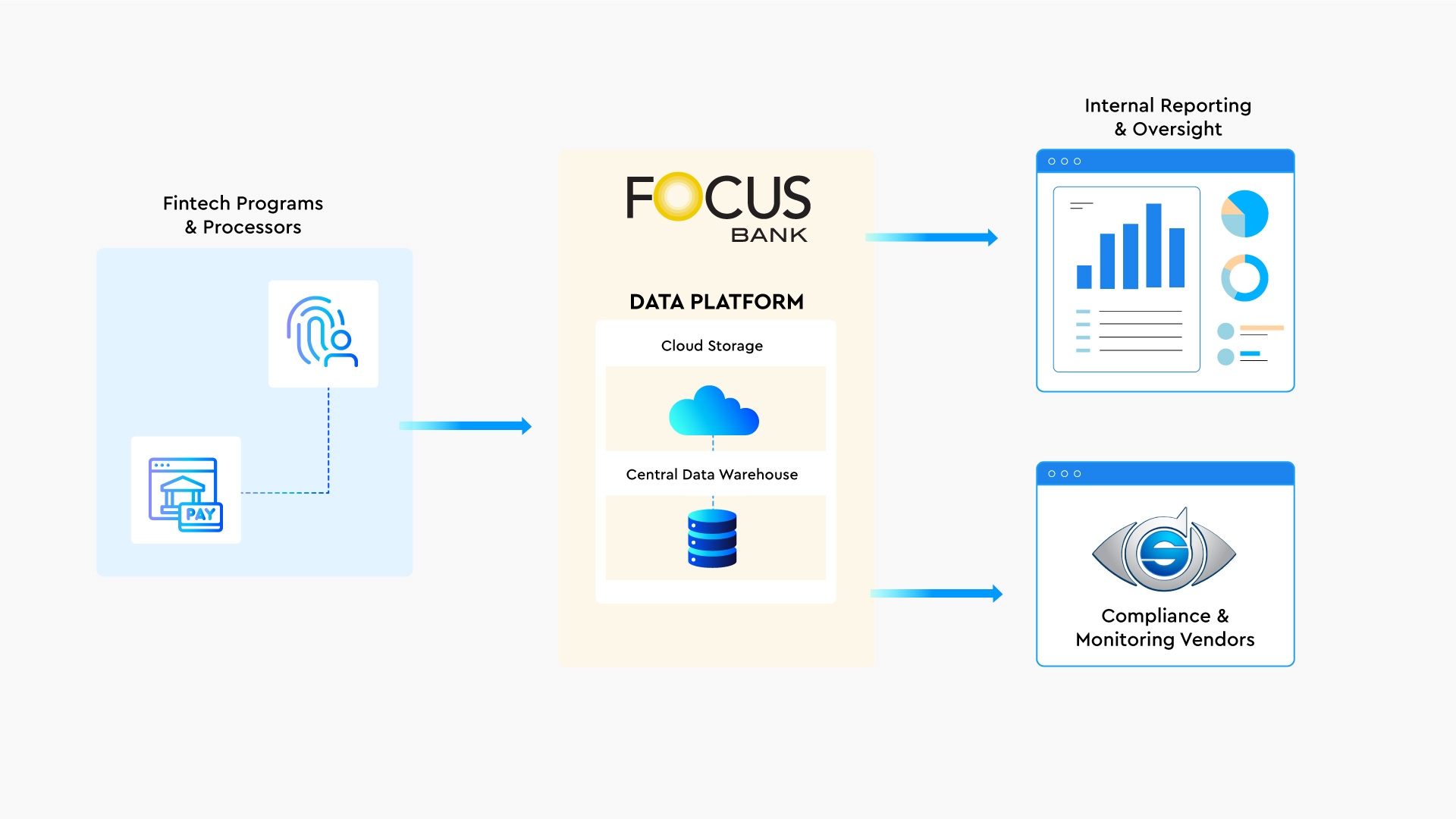

Solution: Planning Data Infrastructure

The first instinct was to build a data lake for the bank’s core systems. That ambition quickly expanded — iDENTIFY would also extract that data and translate it for the fintech side, giving both the bank and its fintech partners a shared, standardized view they could actually analyze.

Designing that shared view raised a question every fintech-sponsoring bank eventually faces: how does the data actually move? APIs are the default answer. But Lee Easton, iDENTIFY’s president, has seen what happens when that assumption goes unchecked. “APIs get talked about like they’re the universal answer, but they don’t magically scale,” Easton said. “Once a fintech is moving millions of transactions a day, relying on APIs as the primary data movement channel starts to show strain.”

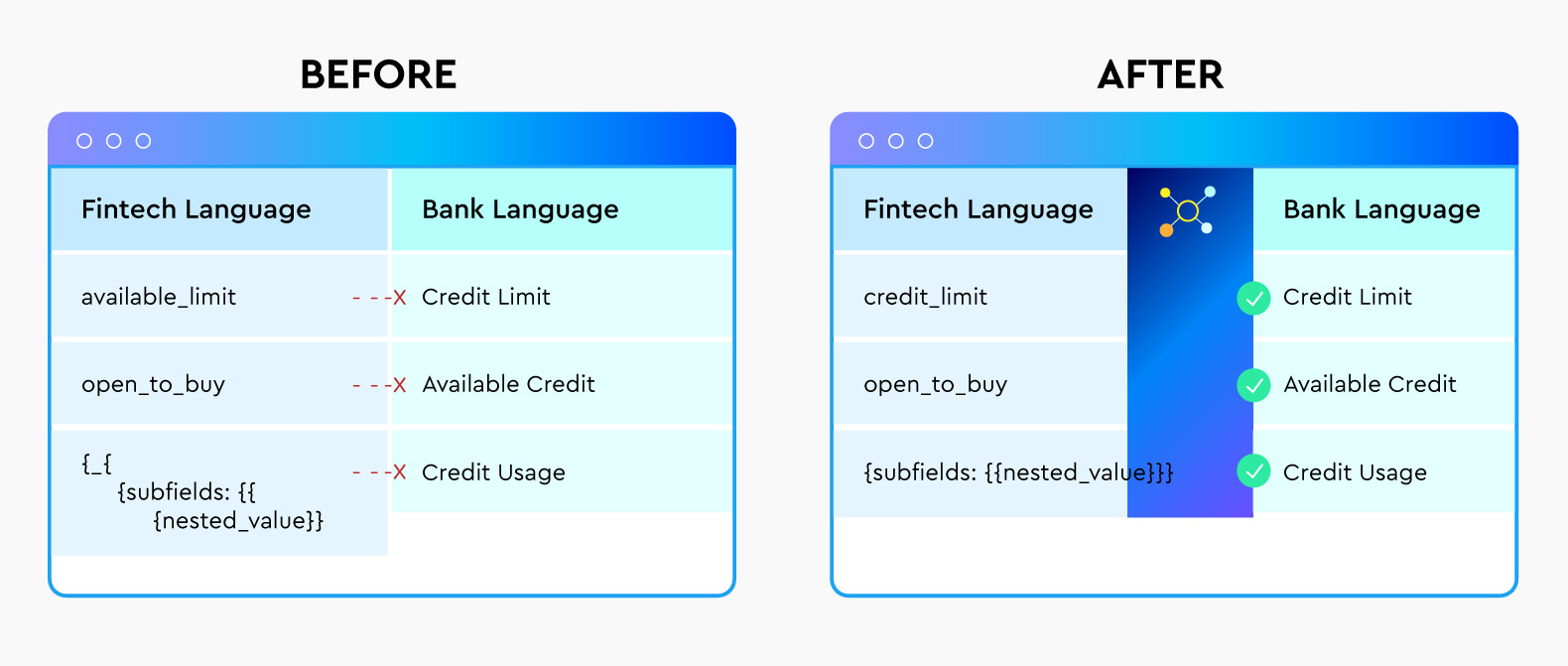

Most of the strain shows up in mapping and reconciliation. One fintech calls a field available_limit, another calls it open_to_buy, and a third buries the same concept inside nested JSON. iDENTIFY builds and maintains the mapping layer that connects those fields to the bank’s definitions and reporting structures — the layer where semantic confusion quietly disappears.

The more sustainable answer is shared cloud environments, like Snowflake or Databricks. When both sides operate on compatible infrastructure, no one has to endlessly ship files or push API payloads across the fence.

It’s also how you kill the spreadsheet monster. Without a normalization layer, teams fall back on CSV dumps, Excel tinkering, and late-night reconciliation fire drills at every month-end.

For Focus Bank, that meant designing the data layer first — so when partners came online, the bank wasn’t reverse-engineering definitions in a spreadsheet.

Outcome: Solving Semantic Disconnects

With the framework in place, Focus Bank brought its first fintech partner online — and the conversations shifted from infrastructure to communication.

Jones described those early reports as trial and error. The bank would request a metric, get back something that didn’t match what they’d asked for, and have to circle back to figure out what the fintech had actually sent.

Working through those disconnects — what each field meant, what each metric was actually counting — became the real work. It’s what ensured both sides defined critical data points in the same terms.

Focus Bank didn’t navigate this alone. FS Vector, the fintech advisory firm that consults with Focus Bank on its partnership program, has watched the same pattern play out across the industry. Jasper Sneff Nanni, a managing principal at the firm, said the strain runs in both directions: fintech partners can end up spending half their time cobbling together ad-hoc data requests instead of building product. The constant back-and-forth, he said, undermines the efficiency and scalability of the partnership on both sides of the table.

Lesson One: Collect the Right Things, Not Everything

The first instinct for banks entering the fintech space might be to hoard data under the assumption that volume equals safety. Focus Bank learned the opposite. Volume just leads to information overload.

The early approach, Jones admitted, was simple: “Well, just give us everything and we’ll sort through what we need and what we don’t need.” It didn’t take long to realize half of what they collected wasn’t useful.

They adjusted from collecting everything to collecting the right things — a tighter target that, paradoxically, made it easier to spot the highest-risk areas instead of drowning in them.

Working with FS Vector, Focus Bank found that effective oversight usually boils down to 15 or 20 metrics that need to land on board decks and in management committees. Everything else is noise.

Lesson Two: Master One Vertical Before Expanding

The leadership team decided to narrow the aperture. They wanted to be excellent at one thing before adding more.

They started with consumer credit, because the leadership and lending teams already knew the regulations and parameters of that asset class. It was the most natural foothold into the fintech space.

In a market that often rewards rapid, unfocused expansion, Focus Bank’s most strategic decision was deliberate restraint.

“We want to be really good at one thing first,” Jones said. “Then, when we know we’re doing it well, we can look at expanding.”

iDENTIFY Helps Banks Understand Their Data

Before any building begins, we take a close look at your current data landscape in our discovery phase.

That means understanding where your data lives today, how your systems communicate with one another, and which integrations already hold your environment together.

From there, we trace the legacy workflows that support your program — the handoffs, the manual steps, the places where risk or inefficiency can hide.

This gives us the clarity needed to document a realistic plan and timeline, along with a preview of the infrastructure that will replace or strengthen what you have now.